The price index for vegetable oils reached a historical high in October. The continued rise in prices has caused consumption to slow down in some categories for both food and non-food uses.

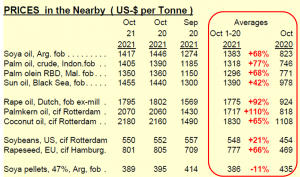

The table below shows the price increases of the main oils over the last 12 months, with many of the oils showing increases of more than 70%.

Similarly, in the last two years, the rise in vegetable oils has been significantly higher than that of other food products, as can be seen in the graph below:

Palm production is affected by the lack of labour in Malaysia. According to Oil World, production has been at least 10% below potential for the last 4 months. Yields in 2021 will be the lowest in 20 years. Annual production is estimated at 17.5-18.5 million tonnes. On the positive side, palm production is expected to grow by 3-4 million tonnes in 2022, mainly in Indonesia and Malaysia.

On the sunflower side, the premium for high oleic sunflower oil has shown a significant increase in recent weeks, partly due to limited offers from major producing countries.

In addition, low premiums offered to farmers have led to lower than expected segregation, mainly in the Black Sea countries. The area of high oleic planted in Ukraine has increased, but a large part will not be harvested as high oleic. Finally, and to add further pressure on prices, the oil content of high oleic seeds appears to be very low.

In order to better understand the dynamics of these and other vegetable oils, we invite you to download and continue reading LIPSA’s market report below, where you will be able to learn first hand:

1. Evolution of reference markets

2. External

3. Balance of major oils

4. Palm oil

5. Lauric oils (coconut and palm kernel)

6. Soybean oil

7. Sunflower and high oleic sunflower oil

8. Rapeseed oil